The Ozempic Economy: How Private Markets Are Betting on GLP-1s

Original post HERE

Jul 08, 2026

Hello to the uninvited.

This is Rosie and Wazz, welcome to Issue 010 of Uninvited.

Roughly 12% of American adults are now on a GLP-1. The Ozempification of the economy has arrived, and the world is eating, drinking and snacking less because of it.

Public markets already had their turn with the story. This week we looked at the private side, to see where the money went.

How Private Markets Are Betting on GLP-1s

The public market version of the GLP-1 trade is pretty well understood by now. Alcohol stocks sold off, food companies got repriced, and Eli Lilly became one of the most valuable companies in the world. JPMorgan estimates these drugs could pull $30 to $55 billion a year out of US food and drink spending by 2030.

The private market story is much newer.

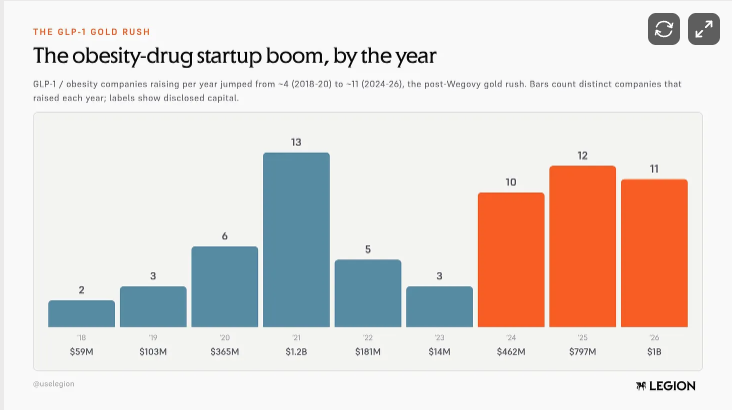

Before Wegovy, obesity showed up in venture portfolios only occasionally, with a few companies raising capital each year. Then the category went vertical. Since 2021, obesity has turned into one of the busiest areas in private healthcare, going from a niche corner of biotech to a steady stream of new companies, products, and business models competing for capital.

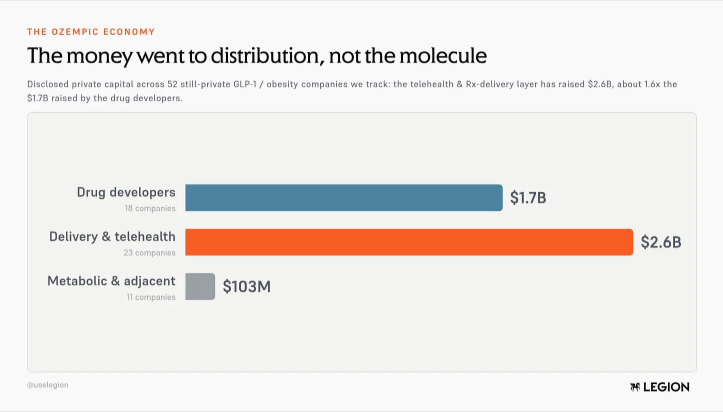

Delivery out-raised the drugs, $2.6B to $1.7B

Of the 52 companies in our dataset, the 22 operating in telehealth and delivery have raised roughly $2.6 billion combined.

The 19 companies developing obesity drugs have raised closer to $1.7 billion.

Private investors are putting more money behind the businesses that get these drugs into patients’ hands than the businesses trying to invent the next generation of them.

Access, prescribing, insurance coverage, side effects, nutrition support, adherence and affordability matter just as much as the molecule itself, and the companies that manage that relationship between the patient and the healthcare system, tend to capture a meaningful share of the economics.

The most valuable weight-loss companies

The valuations point in the same direction.

The most valuable private companies in the cohort are all delivery businesses: eMed and Virta at $2 billion, Nourish at $1.7 billion, SheMed at $1 billion and Noom at $941 million.

The market is paying up for the front door to obesity care.

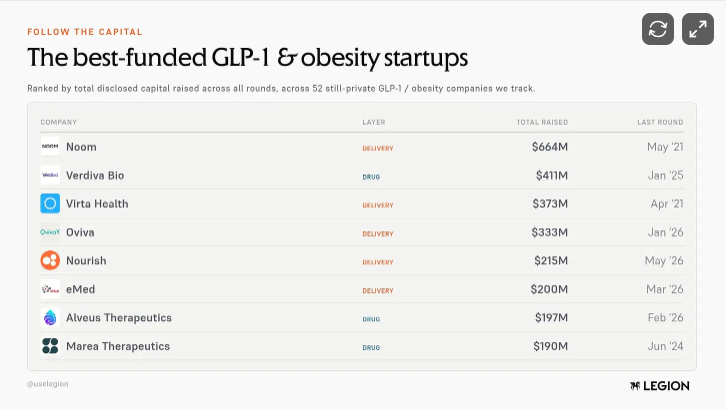

Noom remains the best-funded company in the entire group, with $664 million raised to date, yet its last valuation was set back in 2021 at $941 million and hasn't been revisited since.

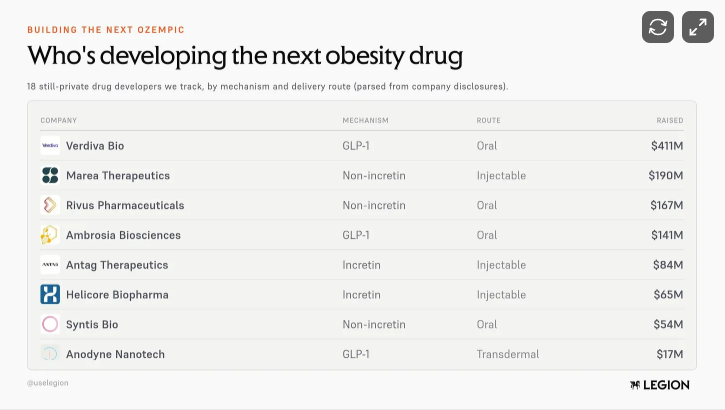

Who’s developing the next obesity drug

The companies building the drugs themselves have raised less capital and attracted less attention, but they are working on a different problem.

Nobody is trying to prove that GLP-1s work anymore. The race now is around better formats: pills instead of injections, patches instead of pills, and fewer trade-offs for patients.

Verdiva leads the category with $411 million raised around an oral GLP-1 program. Behind it are oral and non-incretin approaches from companies including Marea, Rivus and Syntis, alongside Anodyne’s transdermal patch.

If one of those approaches works, the upside looks very different from telehealth or distribution. Better formats come with patents, exclusivity and potentially an entirely new standard of care.

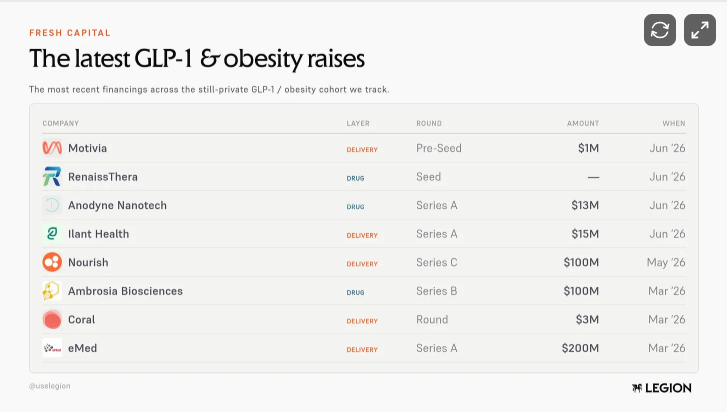

The latest raises: The easy money phase is ending

The latest rounds suggest capital is still flowing into the category, but investors are becoming more selective about what exactly they are buying.

Some companies are focused on access and care delivery, including eMed, Nourish, Ilant, Coral and Motivia.

Others are betting on the next product cycle entirely: Ambrosia with oral small molecules, Anodyne with transdermal delivery and RenaissThera with oral therapies.

The broad GLP-1 halo that lifted almost everything a few years ago appears to be fading. Companies increasingly need a specific problem to solve and a clear place in the value chain.

{kind=link}

The safest bet may not be the drug

For now, private markets seem fairly convinced about where value sits.

In chronic care, the company that owns the patient relationship often ends up owning the economics as well.

That is what makes the delivery layer so powerful. The platforms sitting between patients, prescribers, insurers and pharmacies do not need to perfectly predict which obesity drug wins. If the next standard is an oral GLP-1, a patch, a dual agonist, or something entirely new, they can still be the place patients go to access it.

Drug makers have to be right on the science, the format, the pricing, the coverage and the adoption curve. Delivery companies have a different bet: own demand, then route it to whichever therapy the market chooses.

In a category moving this quickly, that flexibility is starting to look like the asset private investors are really paying for.

Charts by Legion.

If you’re raising, allocating, or sitting on a position that suddenly feels less stable than it did last week, hit reply and tell us what you’re seeing. We read every one.

Uninvited